When you received your Notice of Appraised Value this year, you may have noticed several different values printed on it. Having multiple and different values on the notice can be confusing, especially with regards to the Homestead Exemption and the “homestead cap”. Below, we have attempted to clarify differences between two of these values and to explain how the homestead cap affects these values.

Texas Property Tax Code Sec 23.23 limits increases of the total assessed value to 10% from year to year if the property in under homestead exemption. This 10% increase excludes any improvements added by the property owner. This section does not limit market value increases. Market value is what a property would sell for and can change from year to year based on sales data. The assessed value is used to calculate taxes. Therefore, in some instances you will see two different values on the same property: the market value and the assessed value. The difference in those two values is the Homestead cap loss.

Per the Texas Property Tax Code, all taxable property must be valued at 100 percent of market value as of January 1 each year. This value is shown on your notice as “Market Value” or “Total Market Value”. Because it is based on recent sales, the Total Market Value may change upwards or downwards any amount depending on recent market trends and is IS NOT limited to increases of 10 percent or more. It may change as much as the current market changes.

Per the Texas Property Tax Code, an exemption for taxation is available to an individual’s primary residence. One of the features of the exemption is a limit to the amount that the value for taxation can increase from one year to the next. This limit is frequently referred to as the “homestead cap”. The “capped” value is shown as the “Assessed Value” and is located at the bottom of the list of values on your notice or online. The assessed value IS limited by the Homestead Exemption and may not go up more than 10% in one year in most cases as long as the exemption was in place for the prior year for the current owner. This number is calculated using the previous year’s Assessed Value and a “cap” of 10%. For example:

In 2021, a property with a Homestead Exemption had a market value of $318,138 and an assessed value of $280,084. For 2022, the subject’s market value increased to $462,603, but the assessed value is limited to the previous year’s assessed value ($280,084) plus 10% of that value ($280,084 x 10% = $28,008). The assessed value for 2022 is $308,092. This taxpayer’s value for taxes is starting at $308,092 instead of $462,603 in 2022.

This example would look like the following summary on their 2022 Notice of Appraised Value:

**A residence homestead is protected from future assessed value increases in excess of 10% per year from the date of the last assessed value plus the value of any new improvements. (The limitation takes effect to a residence homestead on January 1 of the tax year following the first year the owner qualifies the property for the residential homestead exemption. [Section 23.23(c) Texas Property Tax Code])

A homestead limitation is a limitation or cap on the amount of value a property will be taxed from year to year. The appraisal district identifies the homestead limitation amount as the “appraised value”. The limitation slows the annual increase of the property tax bill by reducing the amount of value subject to taxation. For residence homesteads, the annual increase is limited to 10% more than the previous year’s appraised value plus and new improvements.

For example: In 2021, a property with the residence homestead has a market value and appraised value of $100,000. Over the next year, prices in the area soar and the appraisal district values the property at $140,000 for the tax year 2022. Since the property had a homestead on January 1, 2021, the appraised value can only increase by 10% plus any new construction. The market value for 2022 would be $140,000 but the appraised value (with homestead limitation) would be $110,000.

Last Year Value + 10% = Current Appraised Value

$100,000 x 1.1 = $110,000

If the property owner added new construction in 2021, let’s say a $20,000 pool, the appraised value would be $130,000.

Last Year Value + 10% + New improvement Value = Current Appraised Value

($100,000 x 1.1) + $20,000 = $130,000

The limitation does not go into effect until January 1, of the following year the property qualifies for the exemption.

Example 1: A property owner purchases their property in December of 2021, and they qualify for their homestead exemption on January 1, 2022. The homestead limitation will no go into effect until January 1,2023.

Example 2: A property owner purchases their property in April of 2022, and they qualify for a prorated exemption, on April 5, 2022. The homestead limitation will not go into effect until January 1, 2024, on year after the January 1 date the exemption qualified.

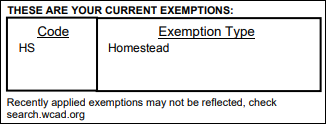

A property with a homestead exemption will have an “HS” code listed in exemptions on the Notice Of Appraised Value and on CAD’s website: Near the top of the WCAD’s notice:

Listed on the property details in WCAD’s online property search. It can be found in two locations:

Other counties’ CADs may have slight variations in reporting.

With few exceptions, Tax Code Section 23.01 requires taxable property to be appraised at market value as of Jan. 1. Market value is the price at which a property would transfer for cash or its equivalent under prevailing market conditions if:

Each appraisal district determines the value of all taxable property within the county boundaries. Tax Code Section 25.18 requires appraisal districts to reappraise all property in their jurisdictions at least once every three years. Tax Code Section 23.01 requires that appraisal districts comply with the Uniform Standards of Professional Appraisal Practice (USPAP) if mass appraisal is used and that the same appraisal methods and techniques should be used in appraising the same or similar kinds of property. Individual characteristics that affect the property’s market value must be evaluated in determining the property’s market value.

The Appraisal Foundation defines mass appraisal as “the process of valuing a universe of properties as of a given date using standard methodology, employing common data and allowing for statistical testing.” USPAP’s Standard 5: Mass Appraisal Development – which applies to appraisal districts performing mass appraisals – states that a mass appraisal includes

Before appraisals begin, the appraisal district compiles a list of taxable property. The list contains a description and the name and address of the owner for each property. In a mass appraisal, the appraisal district then classifies properties using a variety of factors, such as size, use, construction type, age and location. Using data from recent property sales, the appraisal district appraises the value of typical properties in each class.

Three common approaches that the appraisal district may use in appraising property are the sales comparison (market) approach, the income approach and the cost approach.

Sales Comparison (Market) Approach

The sales comparison (market) approach is based on sales prices of similar properties. It compares the property being appraised to similar properties that have recently sold and then adjusts the comparable properties for differences between them and the property being appraised. The sales comparison approach is the valuation method typically preferred in appraising single-family homes and vacant land in mass appraisal when adequate sales data are available.

Income Approach

The income approach uses income and expense data to determine the present worth of future benefits. This approach seeks to determine what an investor would pay now for a property based on its anticipated future revenue stream. The income approach is most suitable for properties frequently purchased and held for the purpose of producing income, such as apartments, retail properties and office buildings.

Cost Approach

The cost approach is based on what it would it cost to replace the building (improvement) with one of equal utility. Depreciation is applied and the estimate is added to the land value. The cost approach is especially useful for appraising properties for which sales and income data are scarce, unique properties and new construction.

Tax Code Section 25.19 requires a chief appraiser to send property owners a Notice of Appraised Value by:

A Notice of Appraised Value is sent if:

A Notice of Appraised Value contains:

Property owners who disagree with the value in the notice, may use the Property Owner’s Notice of Protest included with the notice to file a protest with the ARB.

For additional information on protests and appeals, see Appraisal Protests and Appeals webpage of the Texas Comptroller.

The appraised home value for a homeowner who qualifies his or her homestead for exemptions in the preceding and current year may not increase more than 10 percent per year.

Tax Code Section 23.23(a) sets a limit on the amount of annual increase to the appraised value of a residence homestead to not exceed the lesser of:

Tax Code Section 23.23(e) defines a new improvement as an improvement to a residence homestead made after the most recent appraisal of the property that increases its market value and was not included in the appraised value of the property for the preceding tax year. It does not include repairs to or ordinary maintenance of an existing structure, the grounds or another feature of the property. Tax Code Section 23.23(f) states that a replacement structure for one that was rendered uninhabitable or unusable by a casualty or by wind or water damage is also not considered a new improvement.

The appraisal limitation only applies to a property granted a residence homestead exemption. The limitation takes effect Jan. 1 of the tax year following the year in which the property owner qualifies for the homestead exemption. It expires on Jan. 1 of the tax year following the year in which the property owner no longer qualifies for the residence homestead exemption.

A rendition is a form that may be used by a property owner to report taxable property owned on Jan. 1 to the appraisal district. Both real and personal property may be rendered. The rendition identifies, describes and gives the location of the taxable property. Business owners must report a rendition of their personal property. Other property owners may choose to submit a rendition.

Persons filing renditions who are not the property owner, owner’s employee or affiliated entity or a secured party must have the rendition notarized.

If the total taxable value of personal property is less than $2,500 in any one taxing unit, the property is exempt in that taxing unit.

| ">Rendition Statements and Reports | ">Deadlines | ">Allowed Extension(s) |

| ">Property generally | " data-sheets-numberformat="">April 15 | ">May 15 upon written request Additional 15 days for good cause shown |

| ">Property regulated by the Public Utility Commission of Texas, the Railroad Commission of Texas, the federal Surface Transportation Board or the Federal Energy Regulatory Commission. Tax Code 22.23(d). | " data-sheets-numberformat="">April 30 | ">May 15 upon written request Additional 15 days for good cause shown |

Property Inspection

Penalties